Retirement Income Planning Software for Financial Advisors

Retirement income planning software is supposed to answer one question for your client: will the money be there when I need it? Most tools answer a narrower one—can this person retire?—and then hand you a PDF. The gap between that projection and the portfolio you actually implement is where retirement income planning quietly breaks down.

Here is the pattern. The plan says a client needs $120,000 a year. You export it, open your portfolio system, and build a 60/40 allocation off a risk score. Three months later markets drop, the client calls asking whether they should sell, and you have no fast way to show them that the next several years of spending are already covered. The plan and the portfolio were never connected.

This post is about closing that gap—and what to look for in retirement income planning software for financial advisors who don’t want planning and portfolio construction to live in two different systems.

TL;DR

- Most retirement income software stops at the projection; the portfolio that funds the plan gets built somewhere else, off a generic risk score.

- The better model is pension-style: work backwards from a client’s future spending and match assets to when the money is actually needed.

- Investipal’s liquidity optimization engine automatically builds safe, income, and growth tranches from your models to fund a year-by-year cash flow schedule—then carries that structure into the proposal and IPS.

- You define the model universe; the engine builds the allocation automatically; the advisor overrides or adjusts before anything reaches the client.

- The liquidity analysis runs in about two minutes versus ~30 minutes by hand, and handles annuities and illiquid alternatives natively.

Most RIAs don’t have a planning problem—they have a connection problem

The financial planning category is mature. RightCapital, eMoney, and others do a capable job of projecting whether a client can fund retirement. That’s not the bottleneck.

The bottleneck is what happens after the plan is signed off. The cash flow schedule lives in the planning tool. The models live in the portfolio tool. The proposal gets assembled in a third place. Nothing reconciles automatically, so the advisor re-keys numbers, eyeballs an allocation, and hopes it lines up with what the plan assumed.

When a client asks the only question that matters in a down market—am I going to be okay?—you’re left reasoning from memory instead of pointing at a structure that already accounts for their spending.

Retirement income planning software earns its place when it connects the plan to the portfolio you implement, not when it produces another projection.

The model that actually holds up: match assets to when money is needed

The approach that survives a bad market is the one institutional pension managers have used for decades: start with the future liabilities, then work backwards to fund them. For an individual, the “liabilities” are the client’s spending needs over their lifetime.

That liability-first lens is why retirement income workflows should connect cash-flow timing to asset allocation, not just report a success probability; the Society of Actuaries describes retirement income planning as a discipline that has to account for both spending needs and the uncertainty around funding them.

In practice that means dividing the portfolio into tranches based on when money is needed:

- Safe — covers roughly the first three years of expenses. This is the runway that lets a client ignore short-term volatility.

- Income — covers years four through ten. Built to generate and preserve.

- Growth — years eleven and beyond. This is where long-term return lives, with time to recover from drawdowns.

The point isn’t the exact bucket boundaries—it’s the logic. A client who can see that three years of spending sits in safe assets behaves very differently in a 20% drawdown than one staring at a single blended number. The structure is also what lets you answer the panic call in seconds instead of scrambling.

Investipal’s liquidity optimization engine is built on this logic. We cover the methodology in depth in goal-based portfolio construction; here the focus is the software workflow.

How the retirement income workflow runs in Investipal

1. Bring in the client’s current picture

Start with what the client already holds. Upload a brokerage statement and the statement scanner turns a multi-page PDF into a structured holdings table in about two minutes—cost basis, holdings, and dividends—instead of 30 to 60 minutes of manual entry. Or connect accounts via Plaid. Either way, you have an accurate starting portfolio in minutes.

2. Load the cash flow schedule from your plan

If you already run financial plans in RightCapital, eMoney, or a similar tool, you don’t redo that work. Export the year-by-year schedule of net flows—income minus expenses—and load it in. That schedule becomes the set of liabilities the portfolio has to fund.

If a firm doesn’t run full plans, the same engine accepts a simpler spending sequence: how much the client needs, in which years.

3. Run the liquidity analysis

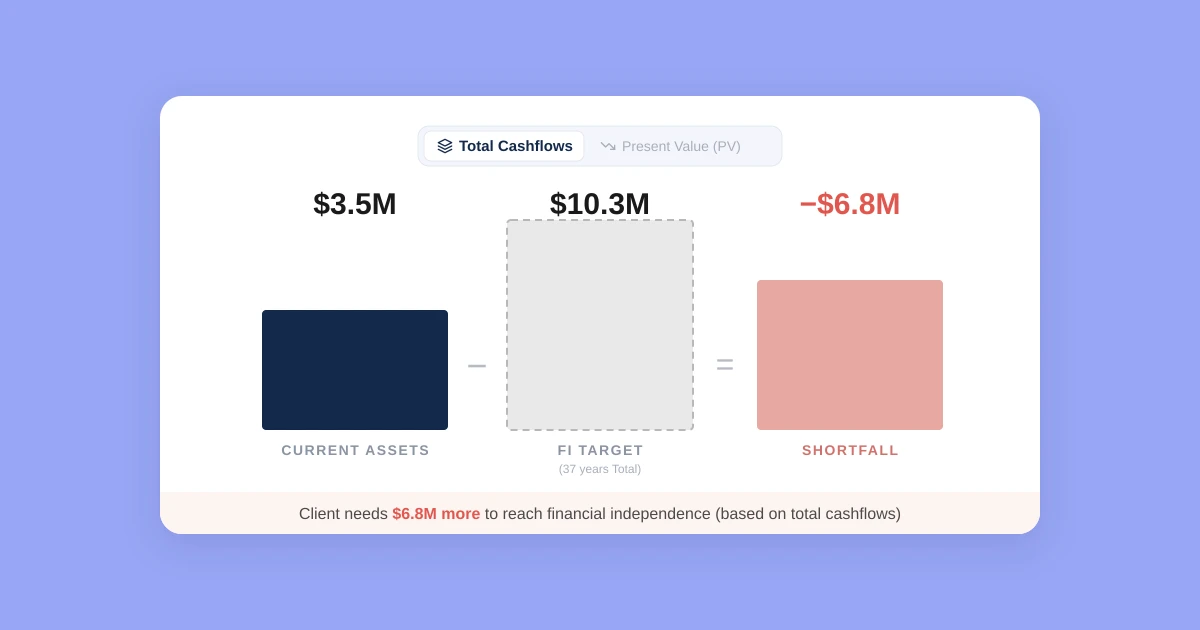

The engine maps the client’s spending needs across the safe, income, and growth tranches and shows where they stand: daily liquid requirement versus what’s provided, contingent reserves, and illiquid allocation versus the maximum you allow. It also runs a financial independence analysis—essentially, does the portfolio put the client in a net surplus position over the plan’s horizon, or does it run dry.

This is where the analysis catches problems early. In one demo with a prospect, an imported account showed a client drawing down so fast against their balance that the system flagged them running out of money in about four years—before a single dollar moved. That’s the kind of finding that’s easy to miss in a spreadsheet and hard to walk back after implementation.

By hand, this analysis takes around 30 minutes. In Investipal it runs in about two.

4. The engine builds the allocation—then you adjust

You define your model universe—a fixed income sleeve, one or more equity models, alternatives, whatever your firm runs. From there the liquidity engine does the heavy lifting automatically: it cross-references the client’s future cash flow needs against your available models and builds the recommended allocation across the tranches—which models fund safe, which fund income, which fund growth.

You get a complete, ready-to-review allocation grounded in the client’s actual liquidity needs, not a blank canvas. Then you override or adjust anything you want before it reaches the client. The engine does the construction and the math; the advisor stays the final decision-maker.

5. Account location for tax efficiency

The engine also helps with where holdings sit. Income-generating assets used to fund near-term spending might belong in a taxable account you draw from first, while growth sits in tax-advantaged accounts. You can model the consolidation—rolling a 401(k), using Roth contribution room—so the recommendation reflects how the client will actually draw income, not just the blended allocation.

6. Carry the structure into the proposal and IPS

Because the liquidity work and the portfolio live in the same place, the proposal comes together in about 10 minutes—comparative analysis of current versus proposed, performance and Monte Carlo projections showing the spending sequence funded across the lifespan, and AI-generated commentary that explains the liquidity strategy in plain language. The matching Investment Policy Statement generates in about 60 seconds. The story the client hears is the same one the analysis told.

Concrete scenarios

The pre-retiree with a plan already in hand. A planning-oriented firm in the Northeast runs every client through RightCapital first. For a couple five years out from retirement, the advisor exported the year-by-year net flow schedule, loaded it into Investipal, and let the engine map it against the firm’s existing model sleeves. The output: a tranche allocation that funded the first three years from safe assets, years four to ten from income, and the balance from growth—plus a clear view of how that allocation shifts over the couple’s horizon. What used to be a manual reconciliation between the plan and the portfolio became a single reviewable recommendation.

The retiree who’s drawing too fast. A solo advisor in the Midwest inherited a prospect’s existing portfolio during a discovery meeting. Loading the holdings and the expected withdrawals, the liquidity analysis showed the spending sequence exhausting the portfolio years earlier than the client assumed. That finding reframed the entire conversation—from “here’s a portfolio” to “here’s the spending rate we need to fix, and here’s the allocation that gets you to a surplus position.”

The client with a pension and a TSP. An advisor near a large employer base works with a lot of clients who have predictable pension income plus retirement savings. For them, the safe tranche is smaller—guaranteed income already covers a chunk of expenses—so the engine leans the recommendation toward income and growth. The liquidity view makes that reasoning explicit instead of buried in a risk score.

These are anonymized composites of real advisor conversations, but the pattern is consistent: the value isn’t a prettier projection, it’s a portfolio that visibly funds the plan.

What to look for in retirement income planning software

If you’re evaluating tools, these are the questions that separate a planning projector from something that actually shortens your decumulation workflow:

- Does it connect the plan to the portfolio? Can you import a cash flow schedule and turn it into an allocation, or does it just project and stop?

- Does it use the money in your models? Recommendations should map to the sleeves you’ve designed—not a black-box allocation you can’t explain to a client.

- Can you override everything? You’re the fiduciary. The software should build the allocation for you and let you override or adjust any part of it.

- Does it handle illiquid assets honestly? Annuities, structured products, and private alternatives should be modeled with real liquidity constraints, and the analysis should show actual versus maximum illiquid allocation.

- Does the output flow into the client deliverables? The liquidity strategy should show up in the proposal and IPS automatically, not get re-explained from scratch.

- How long does an analysis take? A liquidity run should be minutes, not an afternoon.

Where Investipal fits

Investipal is an all-in-one platform for RIAs, and retirement income is one of the workflows it’s strongest at—because liquidity optimization is built in, not bolted on. You define your model universe; the platform builds the client’s allocation automatically to fund their spending needs, flags when a plan doesn’t fund, and carries the structure straight into the proposal, the IPS, and ongoing automated rebalancing. You override or adjust anything before it reaches the client.

The result is less time reconciling the plan against the portfolio, and a much faster answer when a client asks the only question that matters.

FAQ

What is retirement income planning software? Software that helps advisors structure a client’s portfolio around the cash flow they’ll need in retirement. Investipal goes further than most planning tools: it automatically builds safe, income, and growth allocations from your models to fund a client’s year-by-year spending needs, then carries that structure into the proposal and IPS—with full advisor override.

How is this different from RightCapital or eMoney? Those tools model whether a client can retire and project cash flow needs. Investipal takes that output—the year-by-year schedule of net flows—and answers the next question: which portfolio funds those needs. Import the plan’s cash flow schedule and match it to the models you’ve built, so planning and portfolio construction stop living in separate systems.

Does Investipal build the portfolio automatically? Yes—with the advisor in control. You define your model universe, and the liquidity optimization engine automatically builds the recommended allocation across safe, income, and growth tranches to fund the client’s spending needs. You can override or adjust any part before it reaches the client, and ongoing drift is handled with automated rebalancing.

How long does a retirement income analysis take? Once holdings and cash flow needs are in the system, the liquidity analysis runs in about two minutes versus roughly 30 by hand. Statement scanning produces a holdings table in about two minutes, and a full proposal comes together in around 10 minutes.

Can it handle annuities and illiquid alternatives? Yes. Investipal models annuities, structured products, and private alternatives alongside traditional assets, and the liquidity analysis tracks actual versus maximum illiquid allocation so you always know how much liquid runway a client has for near-term spending.

See it on a real client case

The fastest way to judge retirement income planning software is to run one of your own clients through it. Book a demo and we’ll take a real cash flow scenario from plan to liquidity-matched portfolio to finished proposal—so you can see exactly where the connection happens.

.png)