.png)

An Investment Policy Statement (IPS) is the document that keeps an advisor and client on the same page about goals, risk tolerance, and how the portfolio will be managed over time. It is the difference between “trust me” and “here is exactly what we agreed to, in writing.”

Most advisors don’t have an IPS problem in the sense that they don’t know what one is. They have a consistency problem: the largest clients get a polished IPS, everyone else gets an informal version or nothing at all, and the documents that do exist drift out of date the moment a client retires or the market moves. That gap is where compliance exposure and client dissatisfaction quietly accumulate.

This post covers what an IPS is, what belongs in an effective one, the real cost of skipping or neglecting it, and how modern advisors keep one current for every client without burning hours per document.

TL;DR

- An IPS aligns advisor and client on objectives, risk tolerance, asset allocation, and rebalancing rules—and documents that alignment for compliance.

- A strong IPS includes objectives and constraints, risk tolerance and capacity, target allocation with ranges, rebalancing triggers, benchmarks, and a review schedule.

- Skipping or neglecting the IPS creates three risks: misaligned strategies, Reg BI compliance gaps, and client churn.

- The barrier has never been knowing you need an IPS—it’s the time to produce and maintain one for every client.

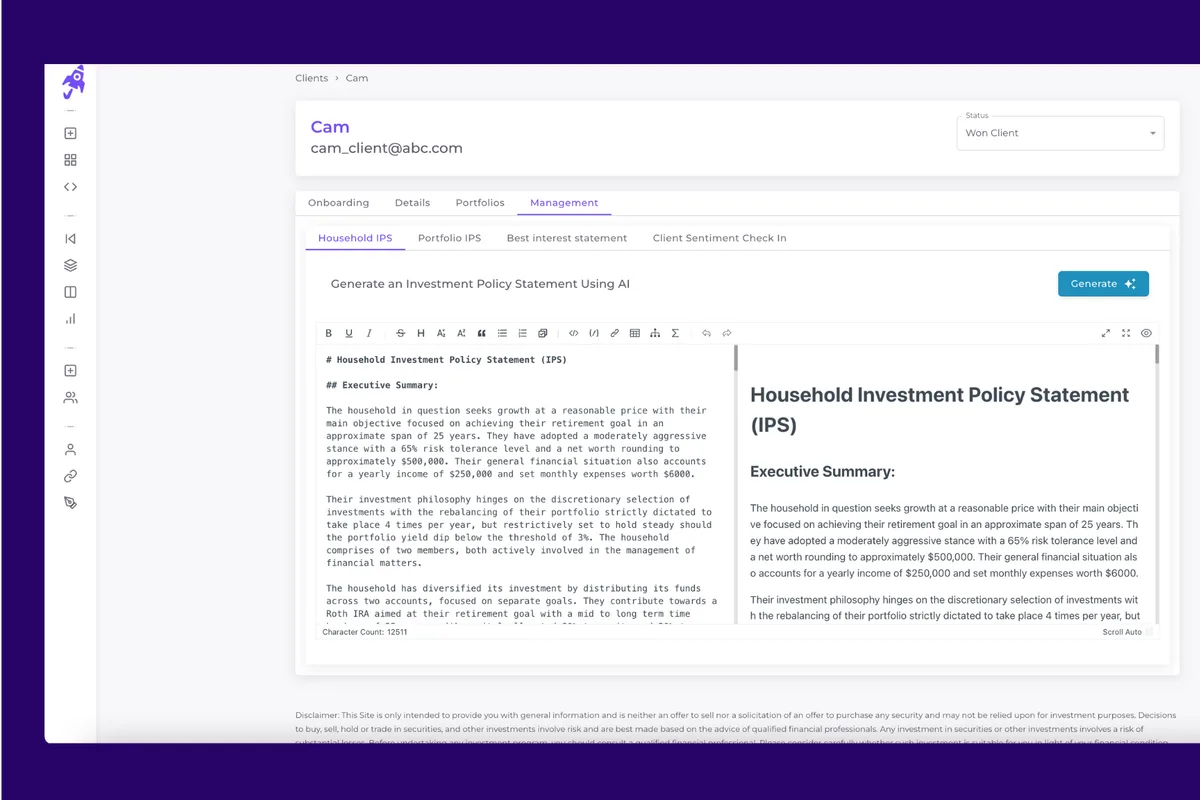

- Investipal generates a compliant, firm-branded IPS from the client’s risk questionnaire in about 60 seconds, down from four to six hours by hand.

What is an Investment Policy Statement?

An IPS is more than a formality. It’s a roadmap that provides direction and consistency in investment strategy. By defining objectives, risk tolerance, and asset allocation up front, the IPS sets a clear, shared understanding between advisor and client that guides decisions through every kind of market.

At its core, the IPS does two jobs at once. For the client, it turns an abstract relationship into a concrete plan they can hold you to. For the advisor, it’s the documented basis for every decision in the account—and the evidence that those decisions were made in the client’s interest.

How an IPS keeps advisors and clients aligned

When goals, risk tolerance, and investment preferences are written down, ambiguity drops. That alignment matters most during volatility, when a client’s instinct to “do something” collides with the long-term plan. A signed IPS lets you point back to what you both agreed to, rather than relitigating strategy in the middle of a drawdown.

What belongs in an effective IPS

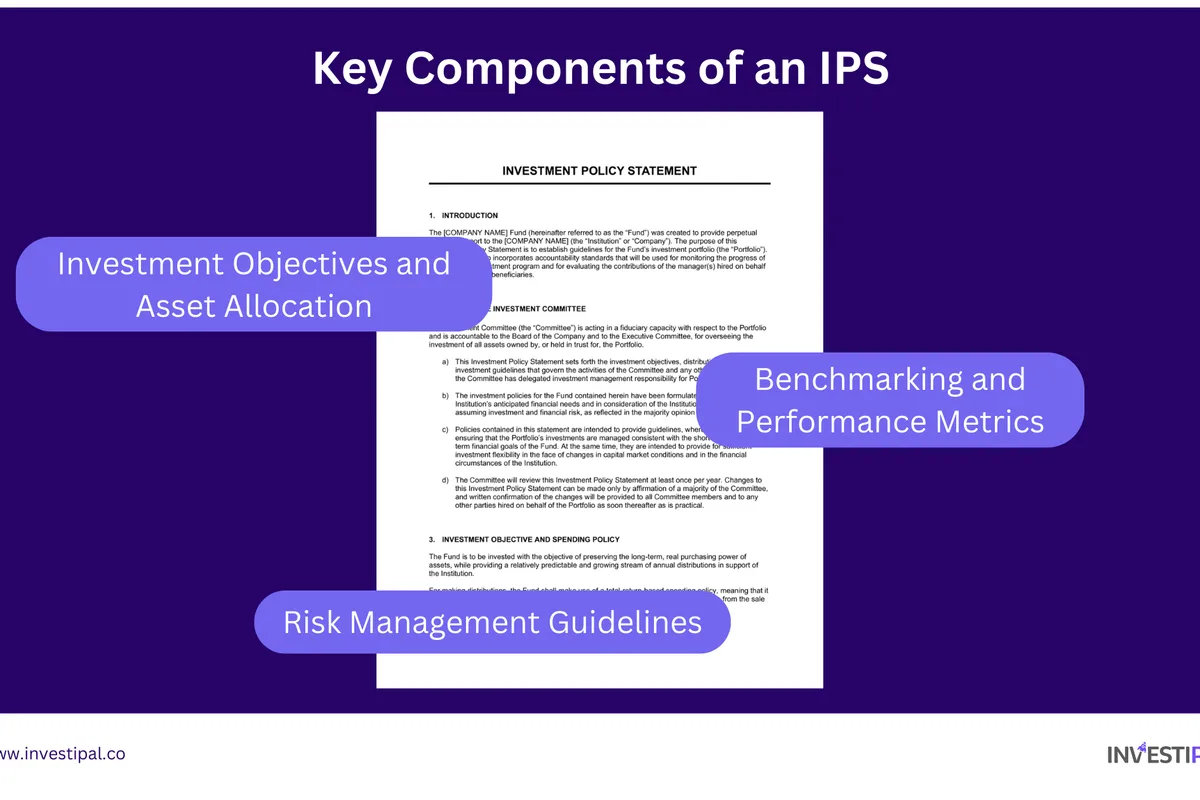

A strong IPS isn’t long for its own sake—it’s complete. These are the components that make it defensible and useful:

- Investment objectives and constraints. The client’s primary goal—growth, income, capital preservation—plus constraints like time horizon, liquidity needs, tax situation, and any held-away positions or restrictions.

- Risk tolerance and capacity. Both the client’s willingness to take risk and their financial ability to absorb it. A digital risk questionnaire makes this assessment repeatable and consistent across the book.

- Target asset allocation with ranges. How the portfolio is diversified to reach the objectives, with acceptable bands for each asset class rather than a single fixed number.

- Rebalancing guidelines and triggers. The thresholds and cadence that prompt a rebalance, so drift is handled by rule instead of by gut.

- Benchmarks and performance metrics. The indices or composites you’ll measure the portfolio against, so “is this working?” has a defined answer.

- Risk management guidelines. Diversification standards, concentration limits, and acceptable-volatility thresholds that keep the portfolio from quietly taking on risk the client never signed up for.

- Monitoring and reporting schedule. When the IPS will be reviewed and how performance will be communicated.

Why the IPS earns its place

A complete IPS pays off for both sides of the relationship:

- It provides a long-term roadmap. With the plan written down, you can hold a disciplined strategy through turbulent markets instead of reacting to headlines. Decisions trace back to the client’s goals, not the day’s volatility.

- It curbs impulsive reactions. A pre-set framework gives clients a reason to stay the course. When markets swing, the conversation is “here’s what we planned for this,” not “what should we do now?”

- It builds trust through transparency. Documenting each part of the strategy shows clients their goals are being managed methodically. That visibility is a retention tool, not just a compliance artifact.

If you want the deeper compliance angle, IPS vs. Reg BI: a financial advisor’s guide to automated compliance documentation breaks down how these documents work together.

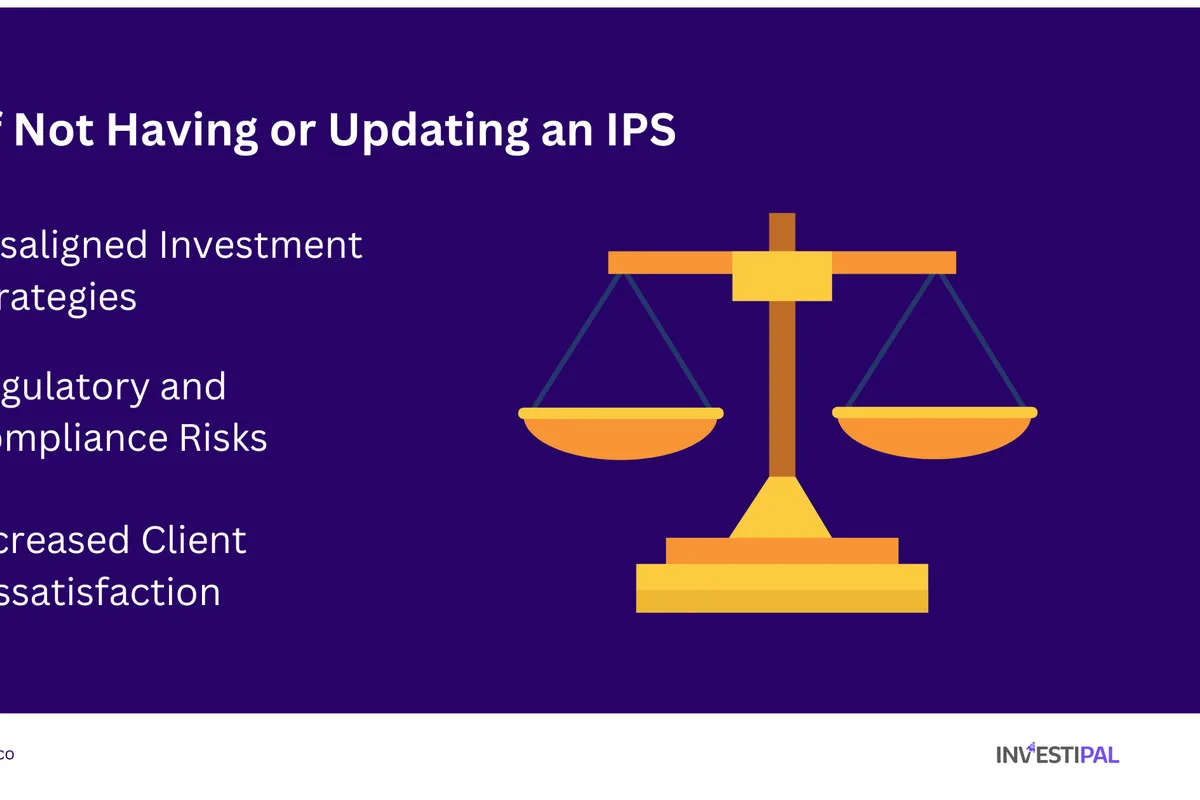

The real cost of skipping—or neglecting—the IPS

Plenty of advisors treat the IPS as paperwork and let it slide. The risks of doing so are concrete:

- Misaligned investment strategies. Without a documented baseline, decisions drift from the client’s objectives and risk tolerance. We hear a version of this constantly about advisors who lean on a handful of cookie-cutter models—the portfolio stops reflecting the individual client, and nobody notices until something breaks.

- Reg BI and compliance gaps. Regulation Best Interest obligates advisors to act in the client’s best interest and document it. An IPS is written evidence that the client’s goals and risk profile were considered. Without one, you’re reconstructing your rationale after the fact—exactly when it’s hardest to defend.

- Client dissatisfaction and churn. An outdated IPS reflects a client who has changed but a strategy that hasn’t. Clients read that as inattention, and inattention is why they leave.

Compliance is increasingly the deciding factor

This isn’t theoretical. The founder of one multi-advisor RIA we worked with recently said the deciding factor in choosing a new platform wasn’t the portfolio analytics—it was the strength of the compliance documentation and the ability to support non-standard holdings cleanly. For firms that are serious about scaling, defensible documentation has moved from a nice-to-have to a buying criterion.

How modern advisors build and maintain the IPS

Creating an IPS is the easy part. Keeping one accurate for every client, every year, is where it falls apart—because doing it by hand doesn’t scale.

That’s the constraint that quietly limits most firms. An advisor at a Midwest RIA put the math plainly: the manual version of producing client documentation took him about an hour per client, where the software version took minutes. Multiply an hour by a full book and an annual review cycle, and you can see why thorough IPS coverage so often gets reserved for the biggest accounts.

Investipal’s IPS tool closes that gap. The same risk questionnaire that profiles the client generates a compliant, firm-branded IPS in about 60 seconds—down from the four to six hours a thorough document takes by hand. Because it’s generated from the client’s actual risk profile and the portfolio you’ve designed, every IPS stays consistent with the rest of the engagement, and producing one for every client becomes realistic instead of aspirational.

For a step-by-step walkthrough, see how to build a compliant Investment Policy Statement in minutes. If you’re evaluating tools, IPS software: 5 critical features every financial advisor needs covers what to look for, and how financial advisors can automate IPS and Reg BI disclosures shows how the IPS fits into a broader compliance workflow.

Best practices for keeping every IPS current

A document that’s never updated is worse than no document—it’s evidence that you stopped paying attention. Keep yours useful:

- Schedule reviews. Revisit each IPS at least annually, and trigger an off-cycle update on material events: retirement, marriage, inheritance, a liquidity event, or a meaningful change in goals.

- Tie updates to the workflow, not memory. Regenerate the IPS when the client retakes the risk questionnaire or when you redesign the portfolio, so the document moves with the relationship instead of lagging behind it.

- Keep it consistent across the book. The same structure for every client makes reviews faster and your compliance file far easier to defend.

- Make it part of onboarding from day one. Generating the IPS during onboarding—alongside the risk assessment and proposal—means the document exists before the first trade, not months later.

Frequently asked questions

What is an Investment Policy Statement (IPS)? An IPS outlines a client’s investment objectives, risk tolerance, target asset allocation, rebalancing guidelines, and performance benchmarks. It’s the roadmap for the advisor-client relationship and keeps decisions consistent across market conditions.

What should be included in an IPS? Client objectives and constraints, a risk tolerance and capacity assessment, target allocation with acceptable ranges, rebalancing triggers, benchmarks, and a monitoring and reporting schedule.

How often should an IPS be updated? At least annually, and any time the client’s situation changes materially. Regulatory and market shifts can also warrant an update.

Is an IPS required for compliance? It isn’t universally mandated, but under Reg BI you must document that recommendations align with the client’s interest—and an IPS is strong written evidence of the goals and risk profile behind those recommendations.

How long does it take to create an IPS? By hand, four to six hours per client. With Investipal, about 60 seconds from the client’s risk questionnaire.

What’s the difference between an IPS and a Reg BI disclosure? The IPS documents the client’s objectives and how the portfolio will be managed; a Reg BI disclosure documents that a specific recommendation was in the client’s best interest. They reinforce each other.

Make the IPS a standard, not a scramble

An IPS is a cornerstone of effective portfolio management—it aligns strategy with goals, supports compliance, and manages risk. Advisors who skip it or let it go stale invite misaligned strategies, Reg BI gaps, and client churn. The reason most firms don’t keep one current for every client has never been a knowledge gap; it’s a time gap.

Investipal closes that gap by generating a compliant IPS in about 60 seconds, so a current document for every client becomes the default rather than the exception. Book a demo to see it generate one from a live client profile.

%20in%20Minutes%20(2).png)

%20What%20Financial%20Advisors%20and%20Broker-Dealers%20Need%20to%20Know%20(1).png)

.png)