Goal-Based Portfolio Construction for Retirement Income Planning

Match spending needs to time horizons — near-term expenses in stable assets, long-term growth compounding untouched. See exactly how many years of spending are covered.

Trusted by advisory firms across North America

Why 60/40 Fails Retirement Portfolios

Traditional allocation ignores the question that matters: "When will I need this money?"

Market drops in early retirement devastate portfolios. A retiree needing $80K next year with that money in equities faces a forced sale during a downturn. Traditional allocation doesn't protect against this.

Mapping spending needs to time horizons, matching assets to liquidity requirements, rebalancing across buckets — that's hours per client in spreadsheets. That doesn't scale to 100 retirees.

"Should I sell?" When near-term expenses are already in stable assets, the answer is simple: "The next 3 years are covered. Stay invested."

How Goal-Based Portfolio Construction Works

Match spending to time horizons and build retirement portfolios around real needs

Define Spending by Time Horizon

Enter annual spending needs or import a cash flow schedule from planning software. Organize into short-term (0-3 years), medium-term (3-10 years), and long-term (10+ years) buckets.

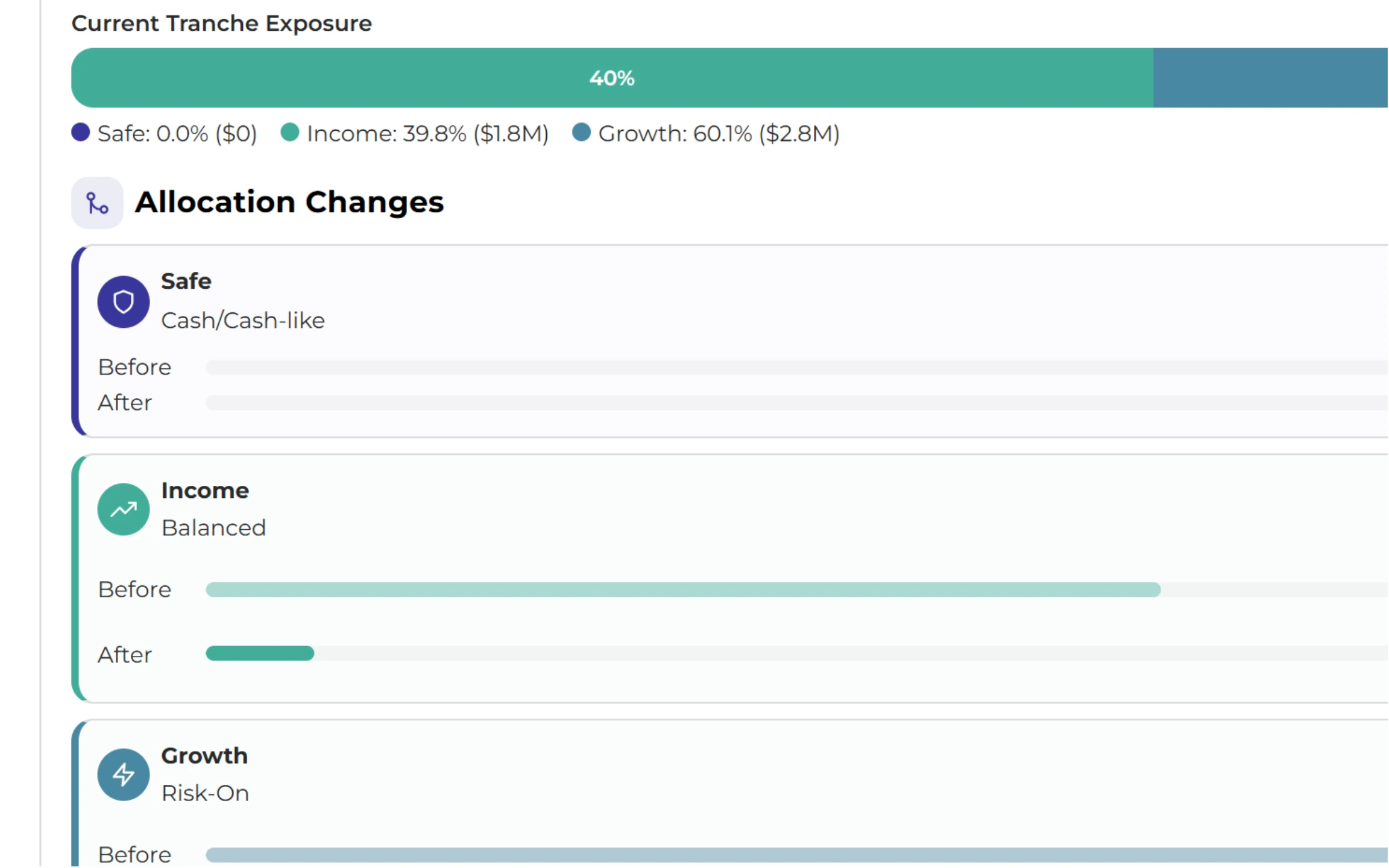

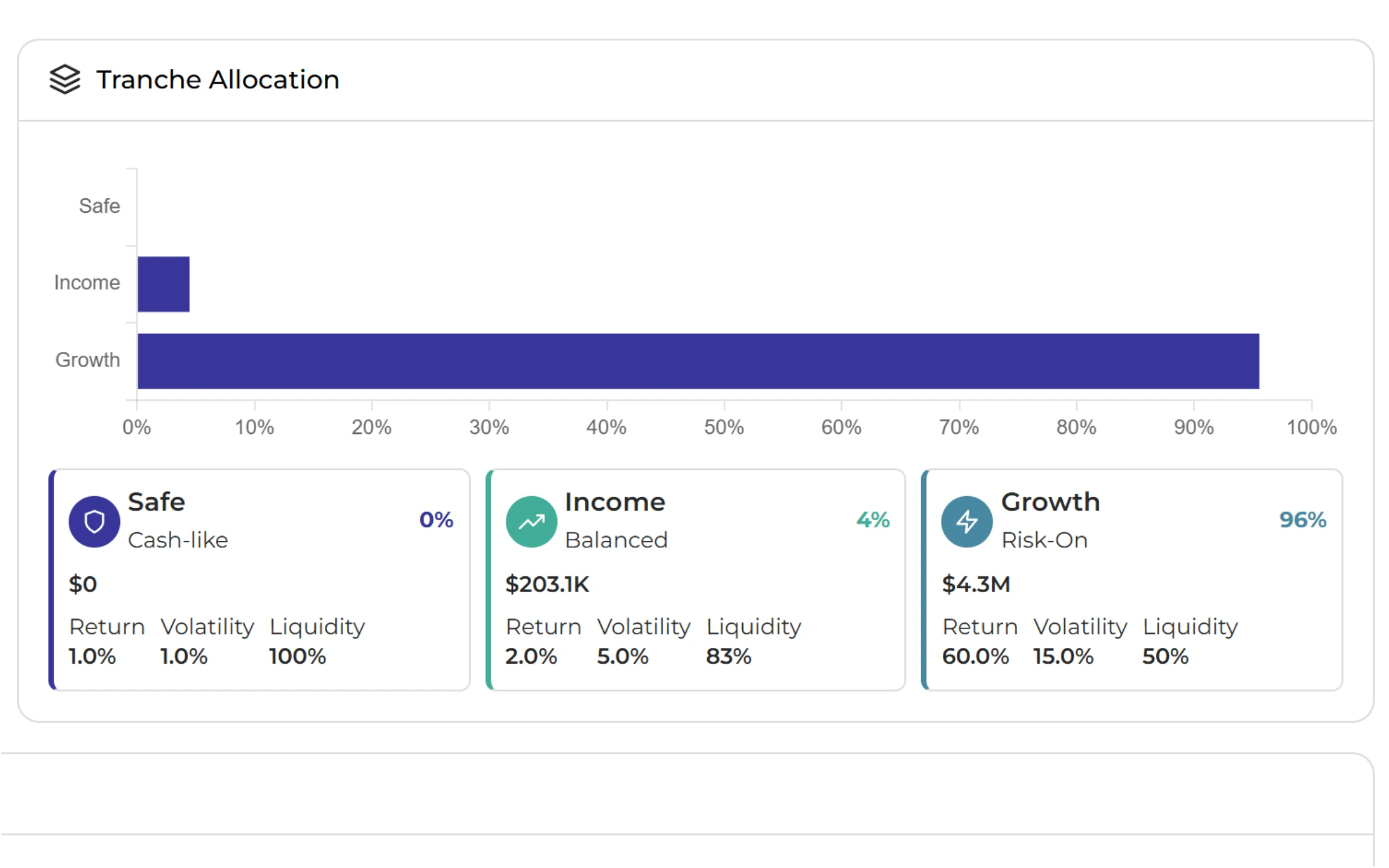

Match Assets to Liquidity Needs

Get a recommended allocation for each bucket based on time horizon and risk tolerance — then edit it. Each dollar sits in the right place for when it's needed.

Personalized Portfolio Construction in Minutes

Build custom portfolios or let the system optimize. Set constraints, select from the model universe, and maximize growth with remaining assets after spending needs are covered.

Track the Liquidity Runway

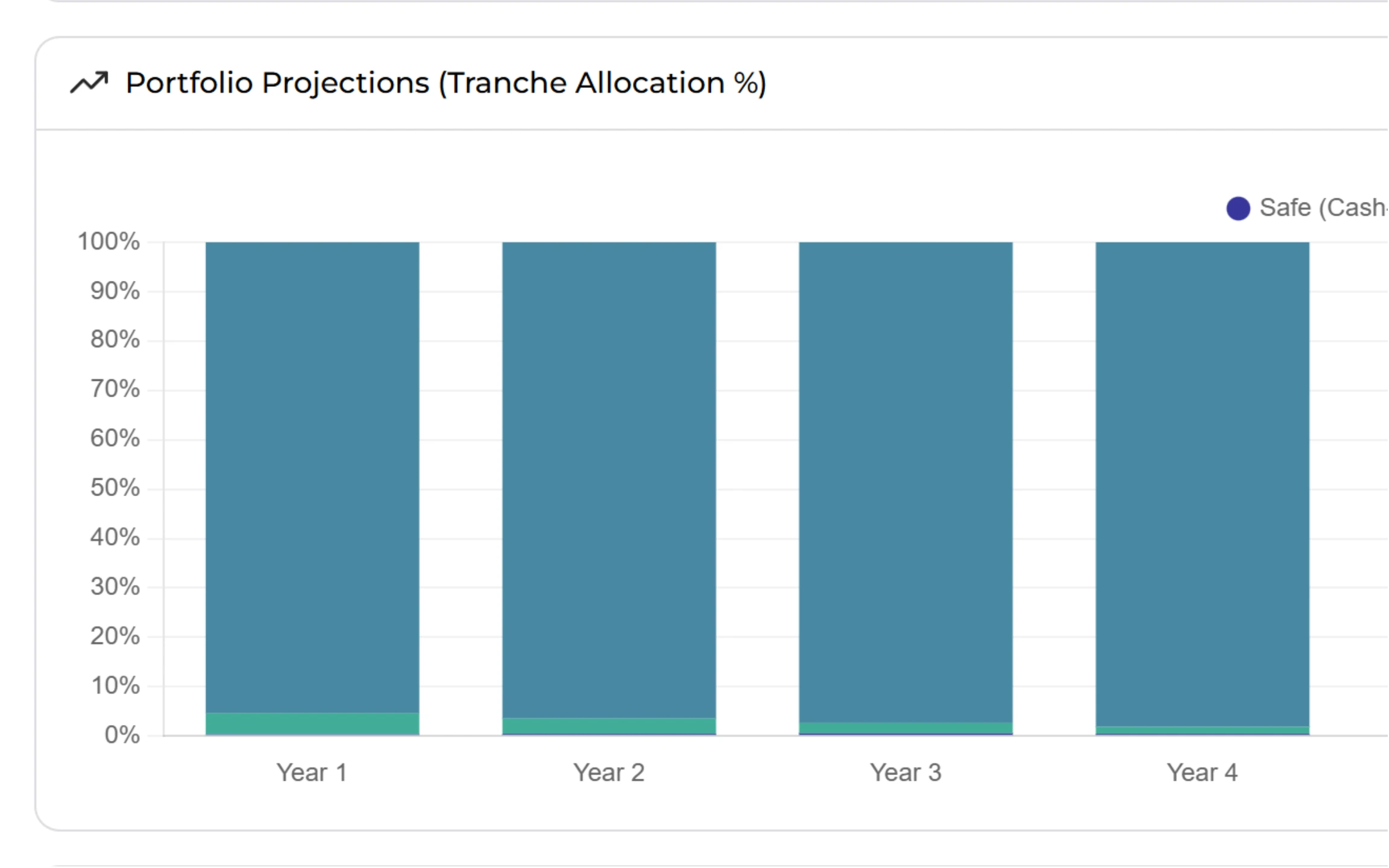

How many years of spending are covered? Which buckets need attention? Clear visualizations answer the real question — not pie charts.

Trusted by financial advisors

See how practices are transforming their workflows

"We're deeply committed to integrating cutting-edge technology to transform the financial planning landscape. Investipal's innovative approach aligns perfectly with our vision, particularly in utilizing OCR technology to streamline processes and elevate the client and advisor experience."

— ProsperPlan Wealth

"Investipal has completely transformed how we approach client onboarding and portfolio management. The AI-powered tools save us countless hours while delivering better outcomes for our clients."

— Pacific Portfolio Advisors

"Investipal has been a game-changer for our firm. It really had become an efficiency multiplier for our assistants and back office. It's an indispensable tool for any advisory firm looking to thrive in today's competitive market."

— William Joseph Capital Management

Frequently asked questions

Common questions answered

See Goal-Based Portfolio Construction in Action

Match assets to spending time horizons and build retirement portfolios clients understand.